Reserve Bank deviates from its economic models in effort to revive the economy.

The Sarb says the destructive effect of the riots will totally negate the stronger-than-expected economic growth achieved in the first quarter of 2021. That the South African Reserve Bank (Sarb) opted to keep the repurchase (repo) rate unchanged at 3.5% last week came as no surprise against the background of sluggish economic growth, low consumer expenditure and the new damage to the economy brought on by the recent unrest in KwaZulu-Natal and parts of Gauteng.

What is of significance is that it also signaled that interest rates are likely to stay lower for longer than anticipated only a few months ago.

In keeping interest rates this low, the Reserve Bank is actually acting against what its own economic models and inflation expectations suggest.

“The Reserve Bank’s Quarterly Projection Model [QPM] predicts higher average CPI [consumer price index] for 2021 and 2023 compared to the May estimate,” says Johann van Tonder, an economist at Momentum Investments.

The QPM forecasts average headline CPI at 4.3% in 2021 (up from 4.2%), 4.2% in 2022 and 4.5% in 2023.

Van Tonder notes that the Monetary Policy Committee (MPC), which sets interest rates, uses the QPM projections as a guide, but the members base their decisions on their own individual assessment of the future path of CPI.

“In this respect, it is noteworthy that the QPM predicted, in May, two increases in the repo rate in 2021 – one in the second quarter [in other words when the MPC met in May] and one in the fourth quarter, but the MPC kept the repo rate unchanged.

“The July QPM predicts a rate increase of 25 basis points in the fourth quarter of 2021 and similar increases in every quarter of 2022. We still foresee the first interest rate increase to occur only in 2022, [as] opposed to the QPM’s prediction of an increase in the fourth quarter of 2021,” says Van Tonder.

Thus, the Reserve Bank actually expected – and its inflation model shows – the repo rate to have increased to 4% by year end and to 5% by the end of 2022.

That the first two of these increases are probably off the table means the increase in the repo rate to 5% has been postponed by more than a year.

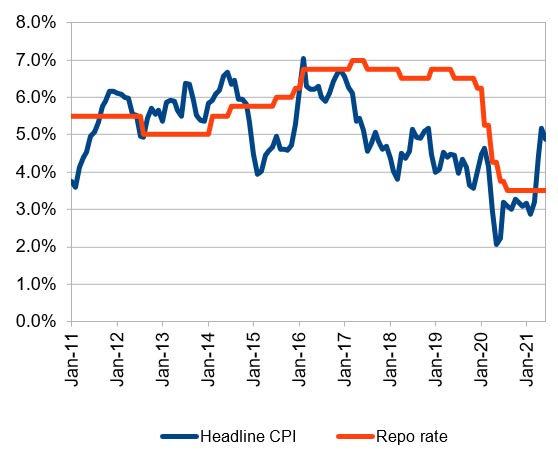

Comparing interest rates with inflation shows that the Sarb was slow in reducing interest rates when inflation started to decrease from the beginning of 2016.

Repo rate and headline inflation

From January 2016 to the beginning of 2020, the repo rate was comfortably higher than the headline inflation rate, offering cash investors positive interest rates.

Source: Data sourced from Sarb and Stats SA

The graph shows the extent to which the Reserve Bank is holding interest rates low, despite the increase in inflation during the last few months.

One of the reasons for this postponement is the effect of recent riots in KwaZulu-Natal and Gauteng on the economy.

The Reserve Bank previously expected that it could increase its estimates for economic growth, but stated at the latest MPC meeting that the destructive effect of the riots will totally negate the stronger-than-expected economic growth achieved in the first quarter of 2021.

“The MPC noted that the unrest and economic damage may have lasting effects on investor confidence and job creation,” says Van Tonder.

“The MPC previously mentioned that the economy’s growth potential could be raised by further ‘derisking’ the economy through stabilizing public debt, providing sufficient electricity for growth, reducing the effect of administered prices on headline CPI and keeping wage increases low.”

We all know what happened to each of these provisos. Civil servants got their salary increases – and a cash bonus. Government finance took a knock from continued spending, such as extending the R350 ‘temporary’ social grant and assisting state-owned insurer Sasria with R3.5 billion.

Slow off the accelerator

Thalia Petousis, portfolio manager at Allan Gray, also expects interest rates to stay lower for a little longer, despite building inflationary pressures.

“The Reserve Bank would likely prefer to support the fragile economic recovery with low rates for as long as prudently possible. Prior to the recent unrest, the Sarb was planning to revise their 2021 growth forecast higher, but say that the impact of the riots has negated the better growth results seen in the first half of the year,” she says, noting that the bank did not change its GDP forecast after all.

“SA’s economic recovery will be delayed due to slow vaccination progress, Delta [and other] Covid-19 variants and riot damage.

“While recent rhetoric coming from the Sarb suggests that neutral interest rates should be closer to 6% to 7%, the process of moving back there will be gradual.

“The Sarb would rather take their foot off the accelerator slowly than slam their foot on the brakes in three years’ time when inflation may have spun out of control,” says Petousis.

While the Sarb’s quarterly projection model suggested a rate hike in the last quarter of 2021, Petousis points to the comment by Reserve Bank Governor Lesetja Kganyago when he asserted that the MPC cannot “outsource” its role to a model.

“If the MPC feel that the model’s suggestions are not appropriate, they will not act on them. Communication from the Sarb suggests that even though its primary goal is inflation targeting, it is also watching SA’s fiscal consolidation prospects and thinking about the role that rates can play,” she says.

Impact on investors

Unfortunately, low rates are bad for investors in cash and money market instruments.

“While SA’s June inflation print at 4.9% is cause for concern for money market investors, keep in mind that base effects are very much at play given that this is a year-on-year calculation,” says Petousis.

“In 2020, our inflation plummeted to just shy of 2%, as economic activity took a nosedive through the unfolding lockdowns. The fact that SA’s policy rates are negative on an inflation-adjusted and forward-looking basis is well acknowledged by Kganyago.

“This means that short-term SA deposits will not fully compensate an investor for inflation erosion until rates are hiked.”

Petousis also warns that inflation is not likely to decline, due to continued increases in administrative prices such as fuel, electricity, water and rates and taxes.

She suggests that investors continually re-evaluate their ability to take on risk, if appropriate to their situation, to get better returns.

“There is no one-size-fits-all. For the extremely risk-averse, it may make sense to stay in a money market fund or in a fund with very low volatility.

“However, for real long-term growth, some exposure to riskier asset classes is essential.”

Original Article: https://www.moneyweb.co.za/news/economy/interest-rates-staying-lower-for-longer/